As you embark on finding the perfect CRM software for your business, you’re likely overwhelmed by the numerous options available. But before you start exploring, take a step back and assess your organization’s specific needs and goals. What are your sales, marketing, and customer service pain points? What features do you need to streamline processes and boost productivity? By understanding your requirements, you’ll be better equipped to navigate the complex CRM landscape and make an informed decision. But where do you start, and what should you prioritize?

Assessing Your Business Requirements

When evaluating CRM software, it’s essential to start by assessing your business requirements.

You need to identify your organization’s specific needs and goals, as well as the challenges you’re currently facing. What’re your sales, marketing, and customer service processes? What’re your pain points, and how do you envision a CRM system addressing them?

Take an honest look at your current workflows, and think about how you can improve them.

You should also consider your team’s size, structure, and roles. Who’ll be using the CRM system, and what features do they need to perform their jobs effectively?

Are there any specific integrations or customizations you require? Make a list of your must-haves, nice-to-haves, and any potential deal-breakers. This will help you narrow down your options and ensure you’re evaluating CRM software that meets your unique business needs.

Evaluating Core CRM Features

Get down to business by evaluating the core CRM features that will drive your sales, marketing, and customer service efforts.

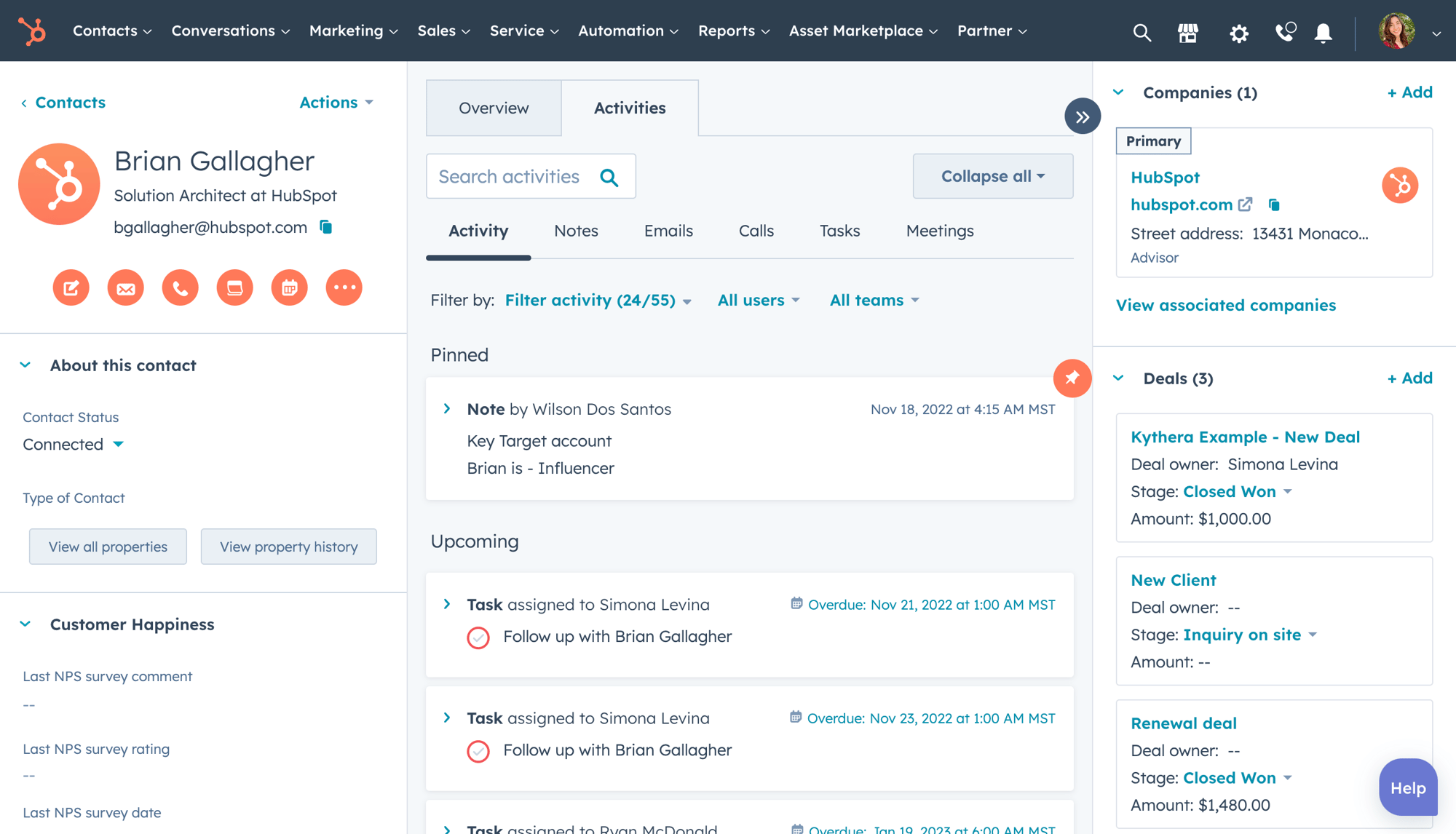

You’ll want to focus on features that align with your business requirements, such as contact and account management, lead tracking, and opportunity management. Consider how the CRM will help you manage customer interactions, including phone calls, emails, and meetings. Will it provide a 360-degree view of customer activity and history?

Next, think about sales performance management features, like sales forecasting, pipeline management, and performance analytics.

You may also need features like marketing automation, campaign management, and social media integration. Don’t forget about customer service and support features, such as ticketing, case management, and knowledge management.

Evaluate how the CRM will help you manage and analyze customer feedback and sentiment. By carefully assessing these core features, you’ll be able to determine which CRM solution is the best fit for your business needs.

Considering Integration and Scalability

You’ve narrowed down your CRM options based on core features, but now it’s time to think about how they’ll fit into your existing tech ecosystem.

This is crucial, as you’ll want your CRM to seamlessly integrate with other tools and platforms you’re already using. Ask yourself: Will the CRM sync with your email client, calendar, and marketing automation software? Can it integrate with your customer support platform and social media management tools?

When evaluating integration, also consider scalability.

As your business grows, your CRM needs to be able to keep up. Will the CRM be able to handle an increased volume of customer interactions, sales leads, and data storage?

Look for CRMs that offer flexible pricing plans, customizable workflows, and robust reporting capabilities to ensure you can adapt to changing business needs.

Don’t underestimate the importance of integration and scalability – a CRM that can’t keep up with your growth will become a bottleneck, hindering your success.

Weighing Cost and ROI Factors

Cost considerations are a crucial aspect of choosing the right CRM software.

You’ll want to evaluate the total cost of ownership, including implementation, support, and maintenance expenses. Consider the pricing model: do you prefer a subscription-based or perpetual license?

Are there any additional fees for customization, integration, or training? You should also calculate the return on investment (ROI) of each CRM option.

How will the software improve sales productivity, customer satisfaction, and revenue growth? What’re the potential cost savings from automating manual processes and reducing errors?

To estimate ROI, consider the costs of your current sales and customer service processes and compare them to the projected costs with the new HubSpot CRM system.

Testing and Implementing CRM

As you narrow down your CRM options, it’s essential to test and implement the software to ensure a seamless transition.

You’ll want to evaluate how the system integrates with your existing workflow, identifies areas for improvement, and addresses any potential pain points.

Start by creating a pilot group consisting of a few team members to test the CRM’s functionality, user interface, and customizability. This will give you a better understanding of how the software will work in real-world scenarios.

During the testing phase, pay attention to the level of customer support provided by the vendor.

Are they responsive to your queries? Do they offer comprehensive training and resources? These factors will significantly impact the success of your CRM implementation.

Once you’re satisfied with the results, it’s time to roll out the system to the entire organization.

Develop a thorough implementation plan, including training sessions, data migration, and workflow adjustments. By doing so, you’ll ensure a smooth transition and maximize the ROI of your CRM investment.

Conclusion

You’ve made it! You’ve assessed your business requirements, evaluated core CRM features, considered integration and scalability, and weighed cost and ROI factors. Now, it’s time to test and implement the CRM software that best fits your unique needs. By following this structured evaluation process, you’ve set yourself up for success. Your new CRM system will help you streamline processes, enhance customer relationships, and drive business growth. Get ready to reap the rewards of a well-chosen CRM!